Decoding the Builder's Financial Health: What the Balance Sheet Reveals

Introduction:

In Blog 46, we established that RERA is a monitoring framework, not a guarantee. It tells you what a builder is reporting. What it cannot tell you is whether the builder has the financial strength to finish what they started.

Think about the last time you tried a new restaurant. You checked the exterior and the reviews. What you didn't do was ask to see the kitchen. Buying an under-construction apartment works the same way. The sales office, the sample flat, and the glossy brochure—these are the dining room. The builder's financial structure is the kitchen. Most Indian homebuyers never ask to see it.

1. Why Financial Due Diligence Trumps Legal Due Diligence

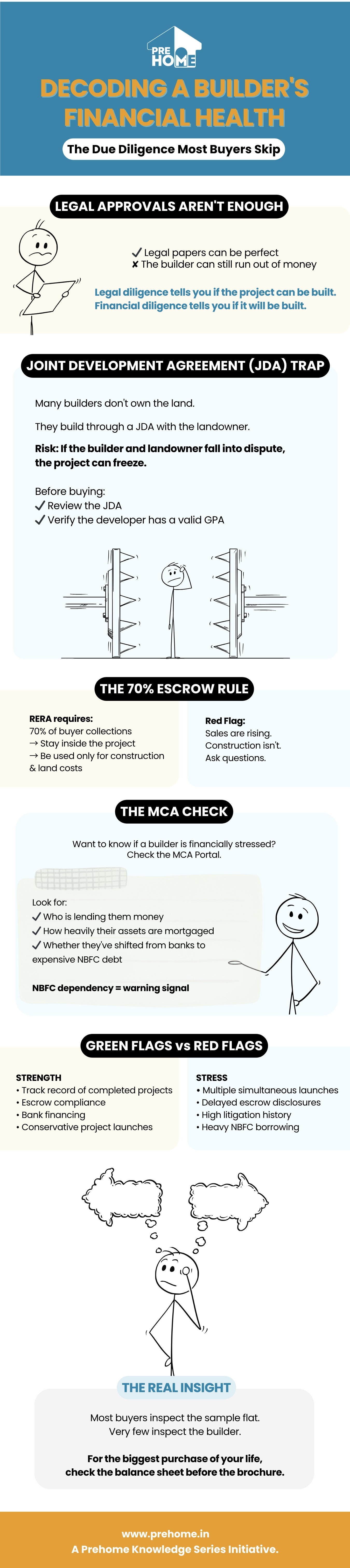

When asked about builder risk, most buyers say, "Their legal papers are in order." Legal compliance is necessary, but India’s real estate history from 2012 to 2020 taught us a brutal lesson: Legally structured projects run by financially distressed developers can still collapse.

-

- The Trap: A developer launches multiple projects in quick succession. They use the advances from Project B to buy land for Project C, while construction on Project A stalls. Each project is legally registered. Each has approvals. And buyers across all three are trapped.

- The Reality: Legal diligence tells you the paperwork is correct. Financial diligence tells you whether the project will actually get built. You must do both.

2. The JDA Trap: When the Builder Doesn't Own the Land

This is one of the least-understood risks in Indian real estate. In metros like Bengaluru, Hyderabad, and the NCR, developers frequently build on land they do not own. They sign a Joint Development Agreement (JDA) with the landowner (e.g., a 60/40 revenue split).

-

- The Risk: If the developer and landowner have a dispute over the revenue split, timelines, or authority, the landowner can seek a court stay. The project freezes. Your money is deployed, but possession becomes impossible.

- The Audit: Before buying in a JDA project, verify two things:

A. Has the JDA document been reviewed by an independent lawyer?

B. Has the landowner provided an Irrevocable General Power of Attorney (GPA) authorizing the developer to sell units and collect payments? A developer who hides JDA documentation is providing its own kind of answer.

3. The 70% Escrow Rule (And How to Verify It)

Under RERA, developers must deposit 70% of all funds collected from buyers into a dedicated project escrow account. Withdrawals are strictly for that specific project's construction and land costs, and must be certified by a Chartered Accountant.

-

- The Audit: Ask the developer for the escrow account details before signing.

- The Red Flag: Cross-reference the RERA filings. If a project is reporting massive sales but construction appears stalled on site, it suggests funds are being collected faster than they are being applied to construction.

4. The MCA Portal Check (Reading the Debt)

This is the most powerful, underused due diligence tool available to the Indian homebuyer. Every corporate entity must file a record of every mortgage or pledge against its assets with the Ministry of Corporate Affairs (MCA). You can see exactly who the developer owes money to in 15 minutes:

-

- Step 1: Go to the MCA portal (mca.gov.in) and search for the developer's registered corporate entity.

- Step 2: Navigate to the "Index of Charges" section.

- Step 3 (The Insight): Look at who is lending them money. Are their assets heavily mortgaged? Have they recently shifted their borrowing from mainstream banks to NBFCs (shadow banks) at extremely high interest rates? When mainstream banks cut a developer off, they turn to toxic NBFC debt just to survive. This is a blaring siren of financial stress.

5. Patterns of Stress vs. Patterns of Strength

No single signal is conclusive. Look for the aggregate picture:

-

- Signals of Financial Stress: Multiple projects launched in rapid succession (cross-subsidization risk), delayed escrow documentation, high RERA litigation history involving fund recovery, and recent high-cost NBFC debt.

- Signals of Strength: A decade of completed projects, current and auditor-certified escrow compliance, financing primarily from mainstream banks, and a conservative project launch cadence.

Checking the JDA structure, verifying escrow compliance, and running an MCA charge search takes a few hours. For the largest financial commitment of your life, that time investment is non-negotiable.

You verified the legal structure and the financial health. Construction is complete. The "Offer of Possession" letter has arrived. And that is precisely the moment when a different kind of surprise appears—one that has nothing to do with fraud, and everything to do with the gap between what was marketed and what was built.

In Our Next Series :

Blog 48: Possession Day — The Hidden Costs and Surprises First-Time Buyers Don't See Coming