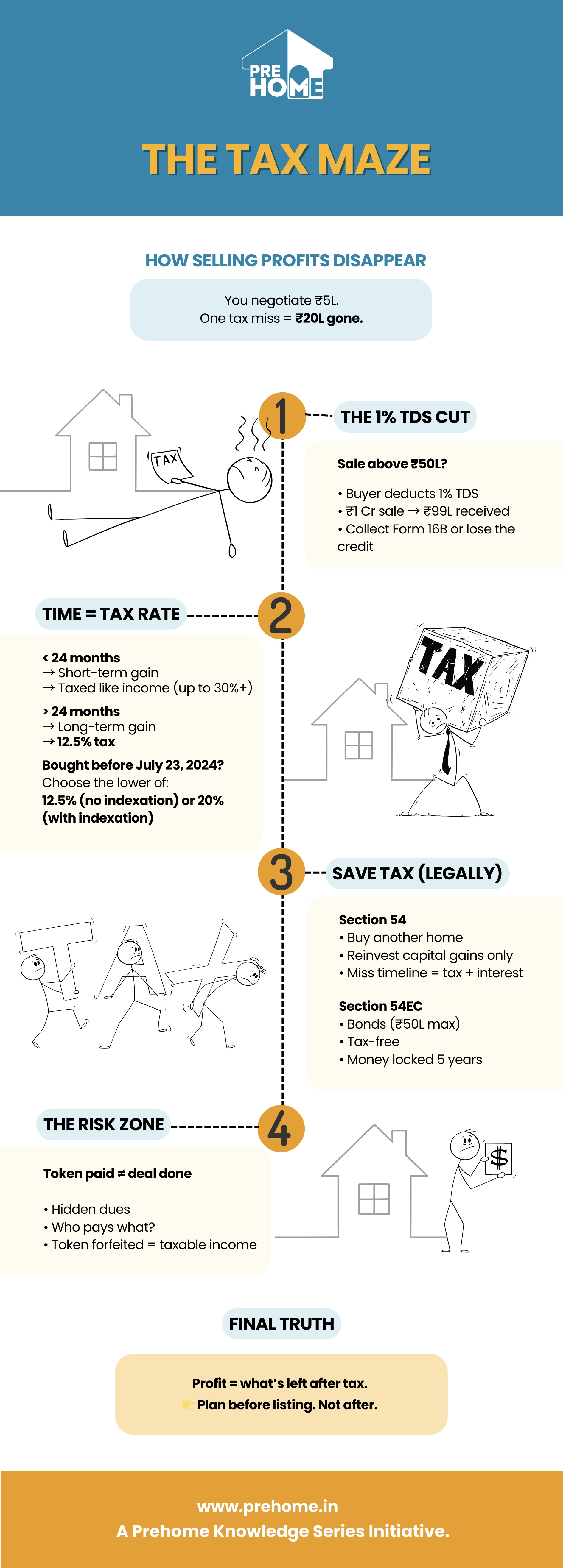

The Tax Maze: Capital Gains, TDS, and the Cost of Poor Planning

You negotiated hard for that extra ₹5 Lakhs in Blog 34. But if you mess up your tax planning, you could lose ₹20 Lakhs to the tax department overnight. Selling a property triggers a complex web of compliance. Ignorance isn’t bliss; it’s a penalty notice.

1. The 1% TDS Shock

This is the most common issue at closing.

-

- The Rule : For any property sold over ₹50 Lakhs, the buyer is legally required to deduct 1% TDS from the total sale value.

- The Cash Flow Gap: If you sell for ₹1 Crore, you will only receive ₹99 Lakhs.

- The Action : Ensure the buyer deposits this TDS using your PAN and provides you Form 16B. You can claim this credit against your total tax liability, but only if the paperwork is correct.

2. Capital Gains Demystified (2024 Budget Update)

Your profit is taxable, but the rate depends on "Time."

-

- Short-Term Capital Gains (STCG) : Sold within 24 months of buying.

- Tax : Added to your income and taxed at your slab rate (up to 30%+). Avoid selling during this period unless it’s an emergency.

- Long-Term Capital Gains (LTCG) : Sold after 24 months.

- The New Rule (Post-July 2024) : The tax rate is generally 12.5% without indexation.

- The Grandfathering Clause : For properties bought before July 23, 2024, you often have the option to choose: 12.5% (No Indexation) OR 20% (With Indexation)—whichever is lower.

- The Insight : Always calculate both. If your property appreciation was low (barely keeping up with inflation), the 20% with indexation method might actually result in zero tax.

3. Tax Leakage Prevention (Section 54 vs. 54EC)

You don't have to pay the tax if you reinvest correctly.

-

- Section 54 (The Upgrade Path) : Reinvest the Capital Gains amount (not the entire sale value) into another Residential Property.

- Timeline : Buy 1 year before or 2 years after sale (or construct within 3 years).

- Trap : If you miss the timeline, the tax becomes due retroactively with interest.

- Section 54EC (The Bond Route) : Don't want another house? Invest up to ₹50 Lakhs in Capital Gains Bonds (NHAI/REC).

- Pro : Safe, tax-exempt.

- Con : Lock-in of 5 years with low interest (~5.25%). This is an "Opportunity Cost." Only use this if you have no better investment options.

4. The "Agreement-to-Sell" Gap

The period between taking the “Token” and signing the “Deed” can be risky.

-

- The Documentation Risk : Ensure your agreement clearly states who pays for unforeseen statutory dues (like pending society levies).

- The Forfeiture Clause : If the buyer backs out, can you keep the token? Usually yes, but it’s treated as income from other sources, not capital gains.

Next in our series:

Blog 36: The Perfect Exit — Negotiation, Closure, and a Dignified Handover